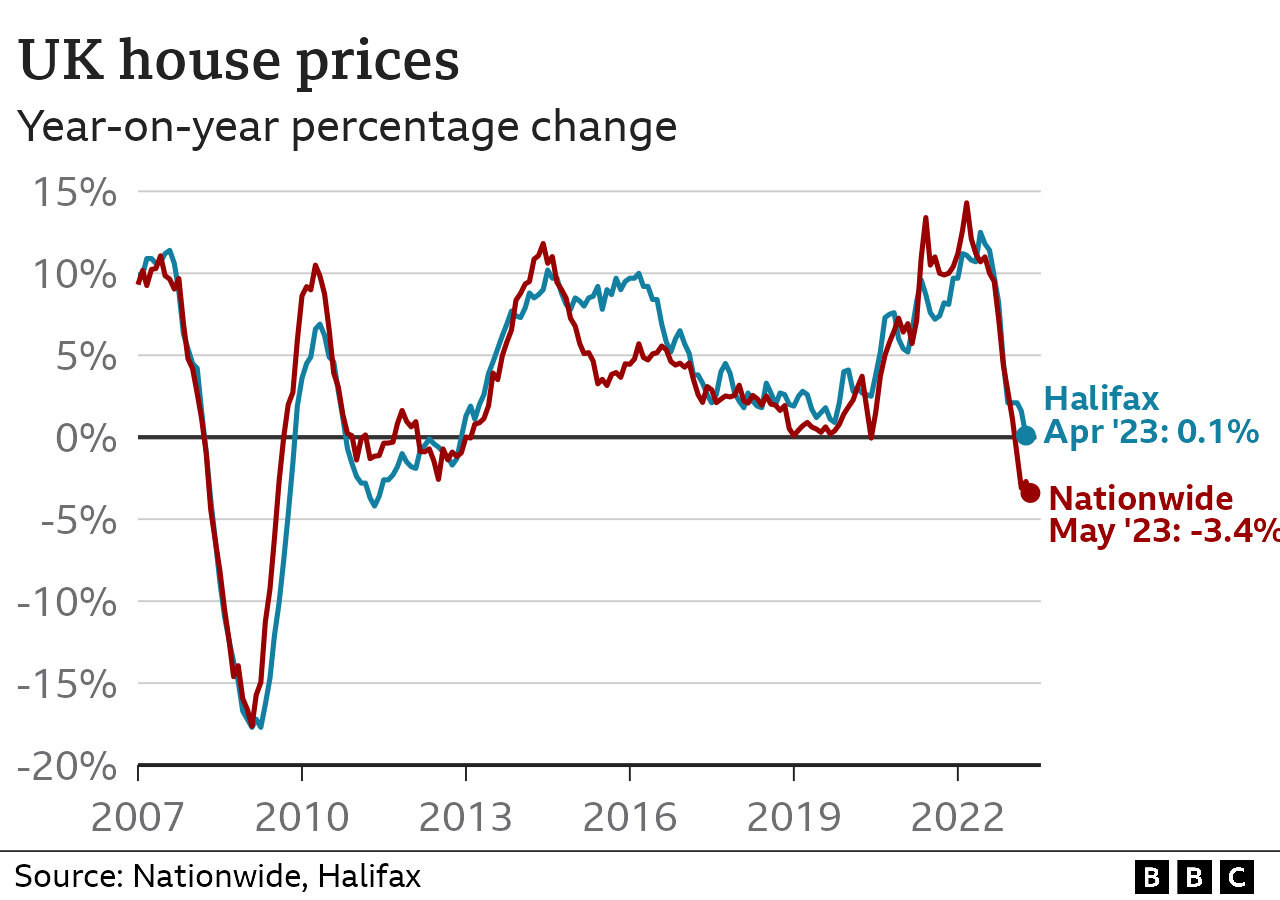

According to The Nationwide, the UK's housing market experienced its fastest annual decline in nearly 14 years in May.

The largest decline in prices since July 2009, according to the building society, occurred in the year to May.

Further increases in mortgage interest rates could harm the housing market, the report also warned.

Mortgage rates recently increased on speculation that the Bank of England would need to raise rates once more as a result of persistently high inflation.

The Nationwide reported as a result that "headwinds to the housing market look set to strengthen in the near term.".

According to the Nationwide, the average home now costs £260,736 after house prices fell by a mere 0.1 percent in May alone.

The average price is still 4% below its August 2022 peak, it continued.

First-time buyers, who have seen home values rise over the past few years despite the pandemic, would typically welcome a decline in housing prices.

The cost of a mortgage has increased beyond what many people trying to climb the housing ladder may have anticipated, however, due to rising interest rates.

Including the time since the start of the Covid pandemic, new data from the Bank of England revealed that the amount of mortgage debt borrowed in April was at its lowest level ever. In total, borrowers paid off their mortgages for £1 point 4 billion more than the banks had lent.

The Bank also reported a decrease in net mortgage approvals for home purchases, from 51,500 in March to 48,700.

The UK inflation rate, which tracks price increases, decreased by less than anticipated in April to 8.7 percent, according to official data released last week. .

According to analysts, the Bank of England will need to increase interest rates from their current level of 4.5 percent to as high as 5.5 percent in order to try and slow the rise in prices.

Following the release of the inflation data, a number of lenders raised their mortgage interest rates. Nationwide made the biggest change, raising rates by up to 0 point 45 percentage points.

The average interest rate for a two-year fixed-rate mortgage is currently 5.49 percent, up from 3.25 percent one year ago, according to financial data company Moneyfacts.

The current rate for a five-year fixed-rate agreement is 51%7%, up from 33%7% at this time last year.

According to data released earlier this week, since last week, nearly 10% of mortgage deals in the UK have been taken off the market.

If you are willing to speak with a journalist from the BBC, kindly include a phone number. There are additional ways to contact us:.

According to Nationwide, interest rates were expected to stay higher for a longer period of time.

According to Robert Gardner, chief economist at Nationwide, "if maintained, this is likely to exert renewed upward pressure on mortgage rates.".

However, he added that given that "household balance sheets appear in relatively good shape" and that "labor market conditions remain solid," the building society was not anticipating a sharp decline in the housing market.

The number of real estate sales has been declining, according to recent statistics. The number of transactions in April was 82,120, which is a 25% decrease from a year earlier, according to data from HM Revenue and Customs released on Wednesday.

According to Sarah Coles, head of personal finance at Hargreaves Lansdown, recent changes in mortgage availability and costs may have "crumbled" confidence in the real estate market.

Despite her assurances that the turmoil that followed last year's mini budget would not recur, she predicted that mortgage rates would increase in "the near future".

We can anticipate that this will lead to decreased demand, fewer sales, and weaker prices. ".

The most recent data on mortgage lending from the Bank of England, she continued, made for "miserable reading.".

It perfectly captures how property sales have stalled at the beginning of 2023. ".

- You are formally in arrears if you miss two or more payments in a row.

- When you ask your lender to change how you pay, such as by making shorter payments, they must do so fairly and take your request into account.

- They might also let you pay only the interest for a specified time or extend the mortgage's term.

- Any agreement will, nevertheless, be recorded on your credit report and may have an impact on your future ability to obtain credit.

Visit this page for more information.