This year, nearly two million households will have their fixed-rate mortgage agreements expire, with the majority likely facing the prospect of higher monthly payments.

What alternatives do borrowers have?

A little over 20% of homeowners have mortgages. tracker or variable rate loans. corresponding to a total of 1 point 6 million households in the UK.

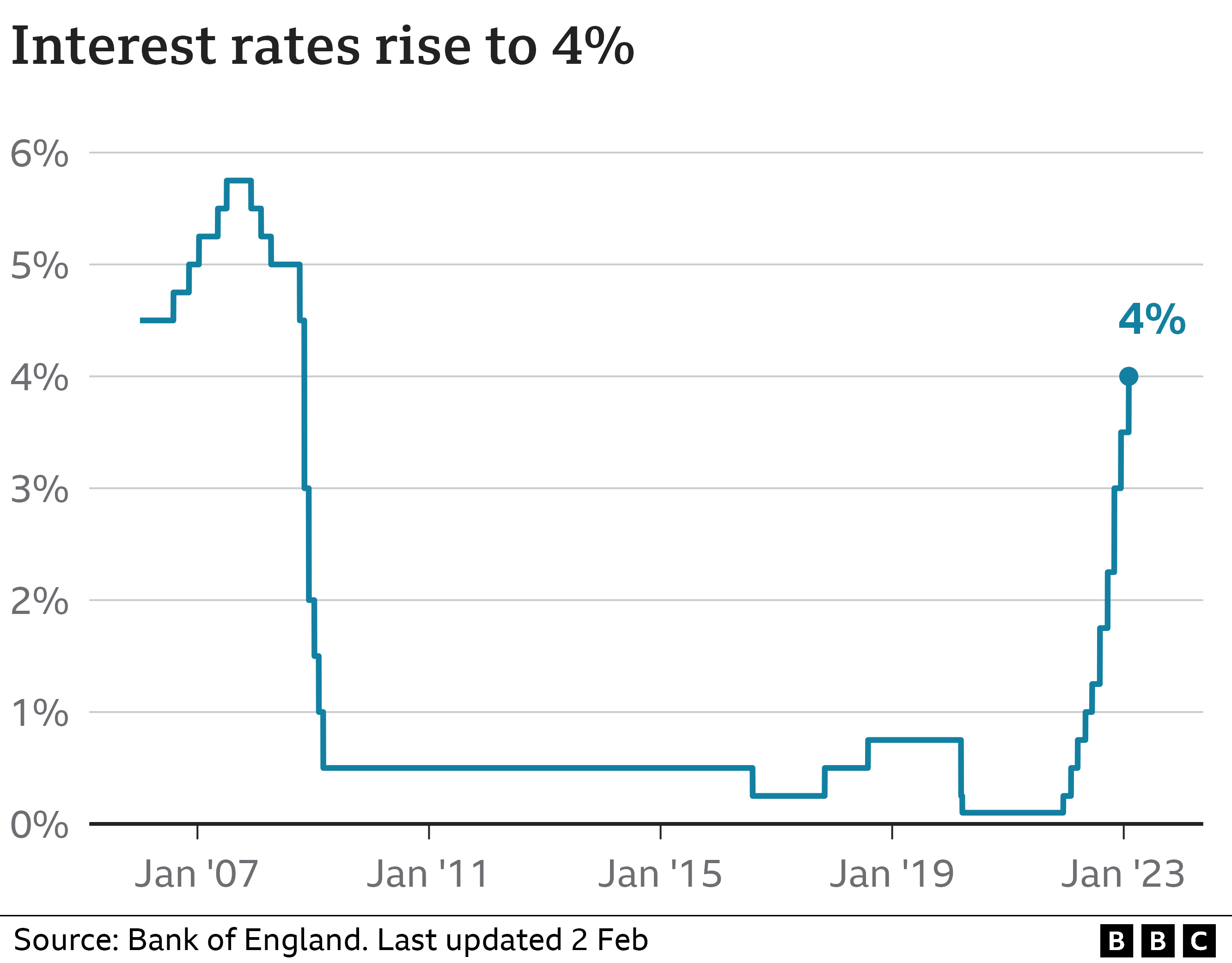

Every time the Bank of England raises its reference interest rate—which it has done ten times in a row—their monthly repayment must increase as well.

In comparison to December 2021, when rates first began to rise, the average homeowner with a tracker deal now pays almost £400 more each month.

mortgages with fixed rates. a different kind. The length of the contract, which is typically two or five years, determines the fixed monthly payment. About 6.5 million homeowners, or 78 percent of mortgage holders, have this type of mortgage.

Borrowers automatically switch to their lender's standard variable rate (SVR) when these deals expire, which is frequently much more expensive. SVRs are typically 7 or 8 percent at this time.

In 2023, 1.8 million fixed deals are anticipated to expire.

The vast majority of borrowers at this point secure a new fixed-rate mortgage from the same lender or a rival. Three-quarters of people use a broker to find a deal.

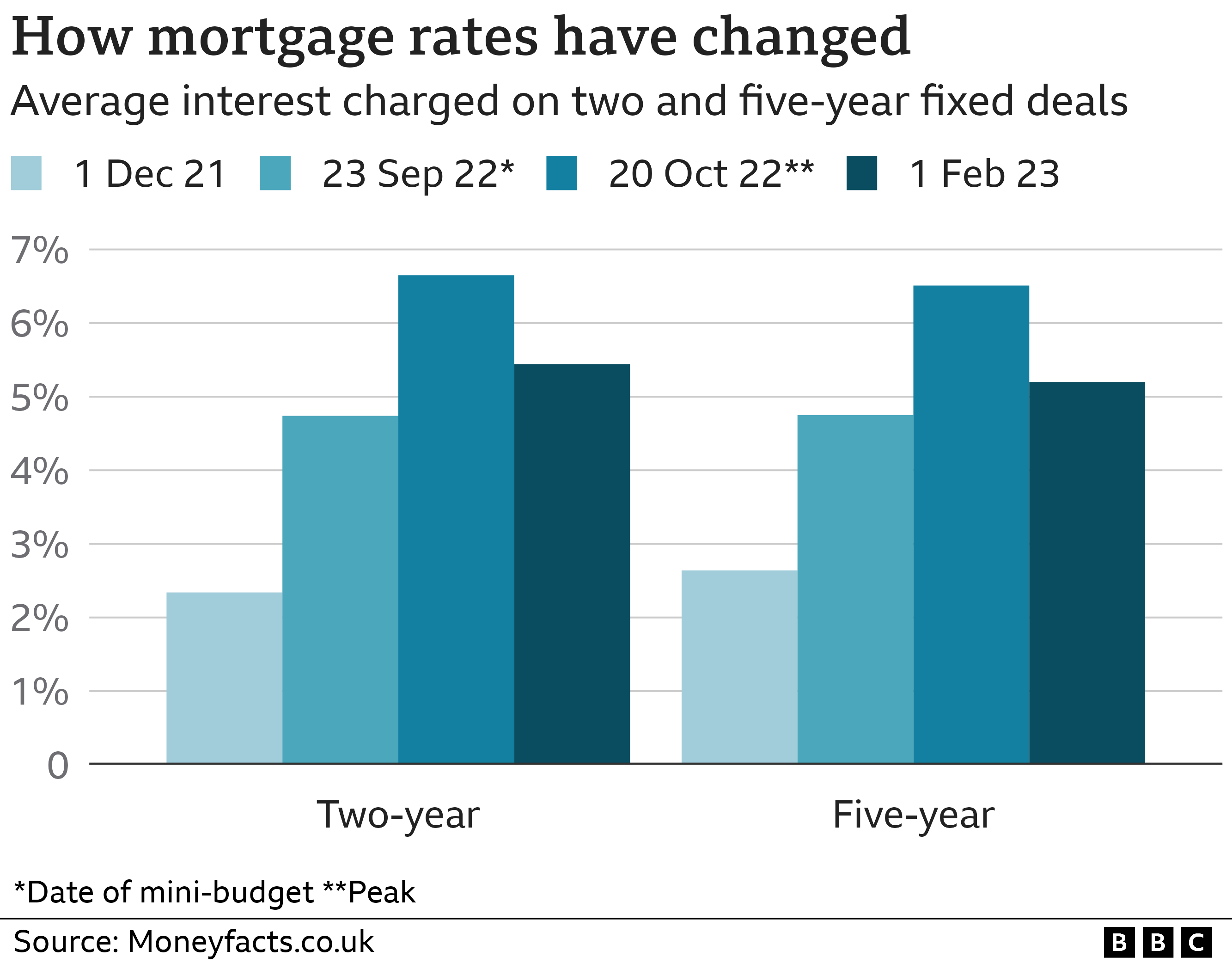

But the fixed-rate offers available today are significantly more expensive than they were in the past. The best offers a few years ago were at 1 percent, but the best rates right now are at 4 percent.

After the mini-budget in September, average rates, which were already rising, skyrocketed but have since fallen back.

Even so, many homeowners could see their monthly mortgage payments increase by several hundred pounds.

Obtain your paperwork. , to verify the date your contract expires and your current interest rate.

Prepare yourself. When your current deal expires, lenders typically allow you to secure an offer within six months. The process of finishing a mortgage offer typically takes at least four weeks. If you wait too long, you risk having to pay the more expensive SVR during the time between deals.

Review your spending plan. decide what you are able to afford. It's possible that since your last mortgage, your circumstances or income have changed. The range of deals is smaller and the processing time is longer as your situation becomes more complicated.

To determine how rising interest rates will impact mortgage payments, use our calculator:.

Click here to view the calculator if you can't.

Consider the cost. Depending on the agreement, there may be exit fees (also known as early repayment charges) or arrangement fees. Ensure that you factor these into your calculations.

Negotiate. Before your new deal begins, but before the lender makes an announcement about lower rates, you can ask it to match the better offer.

During this time, it is possible to switch to a different provider with a more affordable rate, but a new application would be necessary.

The benchmark interest rate set by the Bank of England is anticipated to decline later in 2023, which will have an impact on mortgage rates.

While you wait for more affordable fixed-rate offers to become available, it might be alluring to remain on your lender's SVR.

An SVR is "not a cheap place to sit and wonder," a broker cautions, adding that. A tracker rate might benefit you more. Although trackers can be more affordable than an SVR, they are still connected to the Bank rate and will fall if it does.

You must choose what is best for you, but some brokers contend fixed rates may not decrease enough to make any delay financially advantageous.

Even though it costs more, committing to a fixed rate ensures certainty for a predetermined amount of time.

Some people are already having trouble making their payments on time. Although the level of arrears is still quite low, the head of HSBC warned that "headwinds are ahead of us, not behind.".

Inability to obtain a new deal due to a pattern of missed payments may force borrowers onto the more expensive SVR.

Your credit history, which lenders use to evaluate mortgage applications, may be impacted by other unpaid bills, including credit cards and utility bills.

Before submitting paperwork, verify that your credit report is accurate. Brokers advise being honest about your payment history.

You might think about making your mortgage term longer. For instance, if your mortgage is scheduled to be repaid over 17 years, it can be restructured to be paid off over 20 years.

That lowers monthly payments and may be a temporary solution for some people. Over the course of the mortgage, it will ultimately result in higher interest payments.

Anyone whose income turns out to be higher than anticipated could use the extra cash to pay off their mortgage sooner than planned. Most lenders let you do this up to a certain point, which would reduce the overall interest expense.