The dinner party circuit and the golf course are no longer the only places where mortgage rates are discussed.

At the entrance to the school or in the supermarket, people are chatting with friends about their mortgage shock. Tenants are concerned that their landlords will raise their rent as a result of higher rates facing them as well as nervous homeowners.

Here are five explanations for the current uproar.

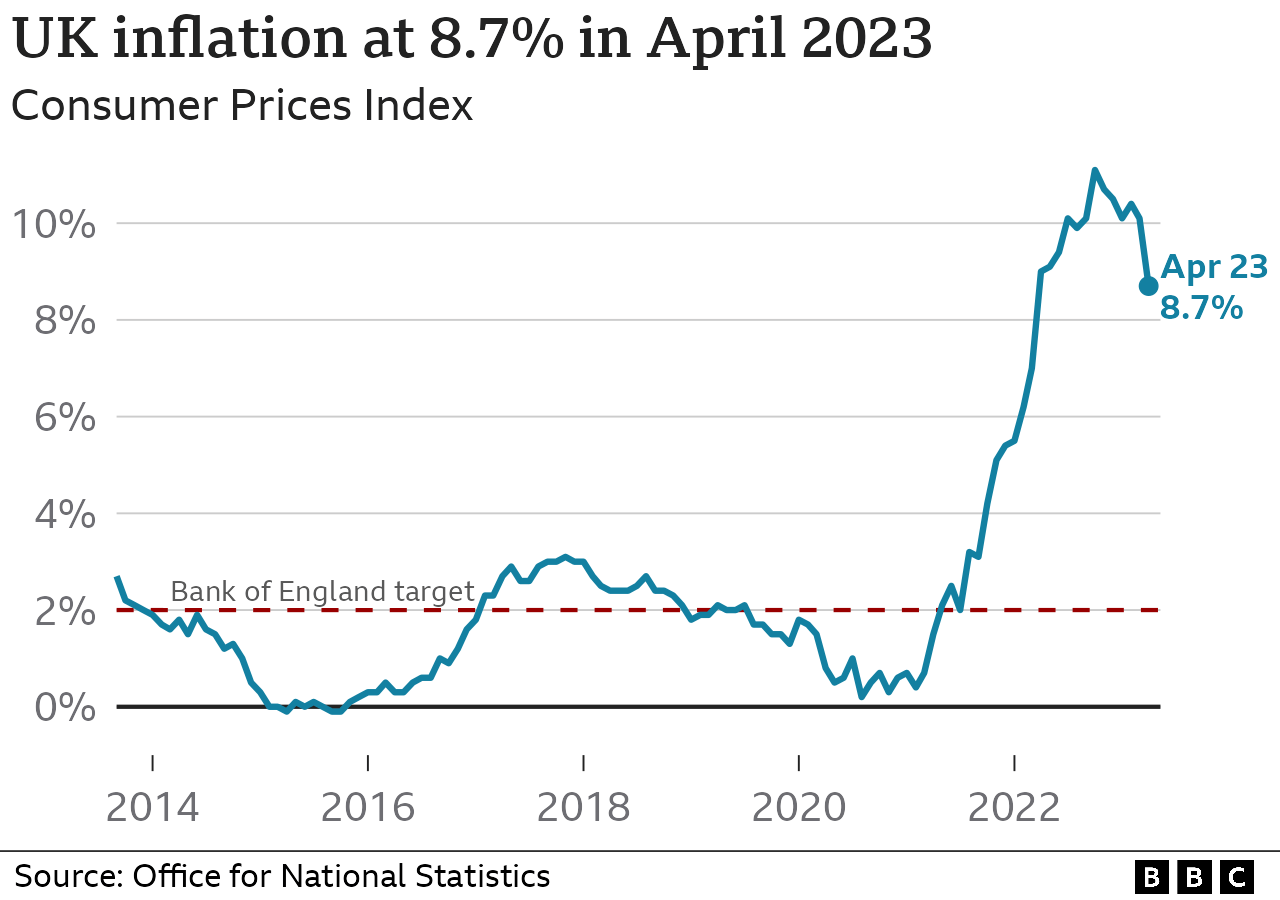

If predictions are to be believed, price increases should have significantly slowed down by now. The rate of inflation charts the increase in living expenses by displaying the rate at which prices are rising.

Though it appeared that inflation would remain high for a longer period of time than anticipated, the most recent official data alarmed the markets and lenders. It also alluded to the hypothesis that rising prices were becoming more deeply ingrained in the UK economy.

The Bank of England's decision to raise interest rates is its most important, if somewhat blunt, strategy for combating high inflation. Lenders would incur higher costs as a result of the benchmark rate's anticipated peak at 5 point 5 percent rather than the current 4 point 5 percent, so they have increased the interest rate they charge for mortgages.

President of Queens' College at Cambridge University and a former deputy director of the International Monetary Fund (IMF), Mohamed El-Erian, claims that central banks should bear the responsibility for their predictions that high inflation would only be transient.

It turned out that inflation was persistent, which meant that both central banks and society as a whole were slow to prepare for higher inflation, he told the BBC.

When tax breaks provided by ministers to keep the housing market humming during COVID were ending, there was a rush from homebuyers two years ago.

The equivalent tax in Scotland and Wales, as well as lower or zero rates for stamp duty, analysts claim "made a hot market even hotter.". Due to the pandemic and the reduction in stamp duty, many people had to relocate quickly.

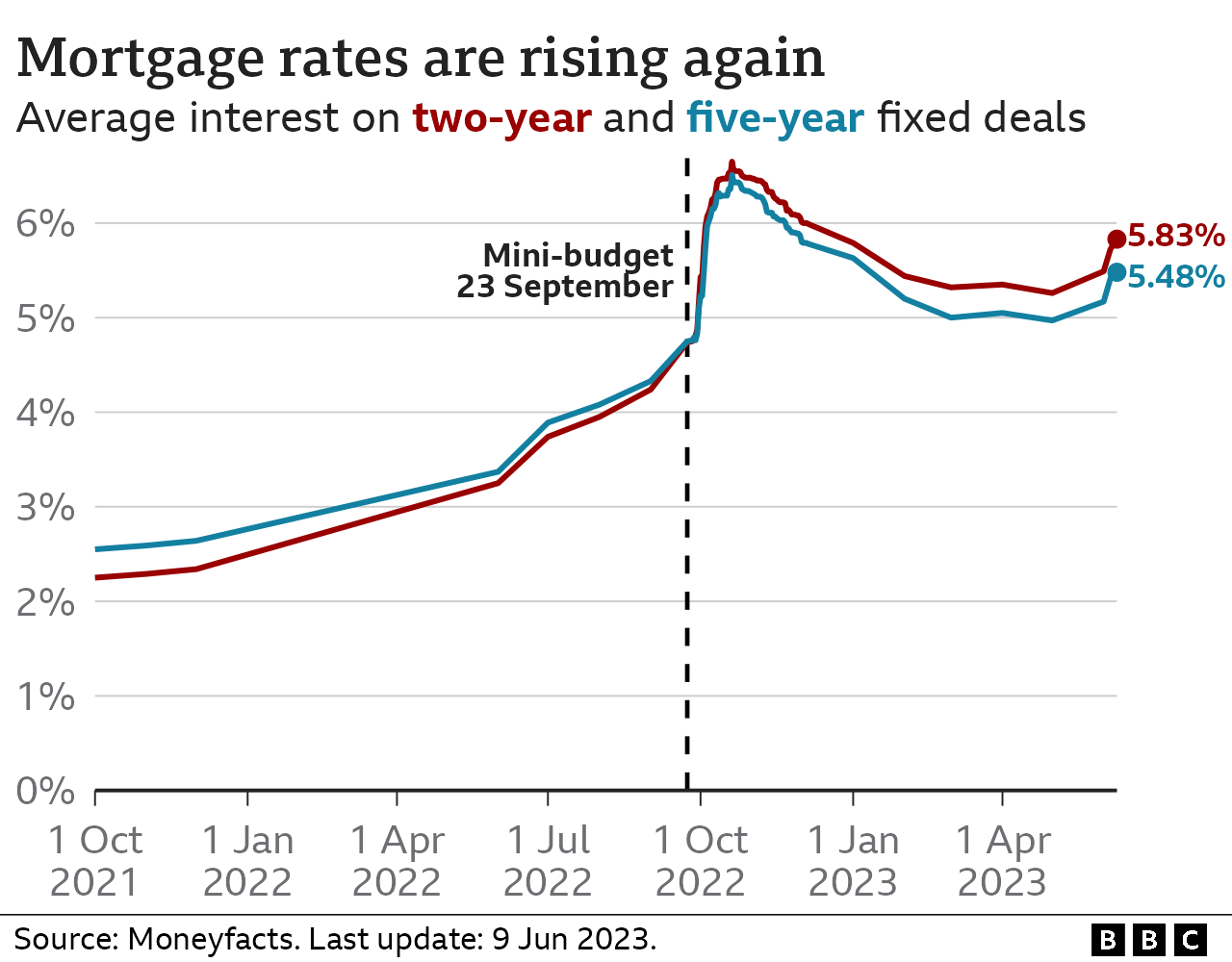

Numerous of those purchasers received two-year fixed-rate mortgages, which are now about to mature.

According to data from the City watchdog, the Financial Conduct Authority, the peak period for homeowners exiting fixed mortgage deals this year is from July to October, when more than 400,000 are anticipated to do so.

The timing could be better. The rates offered for a new deal today are significantly higher than they were then. A monthly mortgage payment could increase by several hundred pounds as a result.

Solihull residents Anil and Jessica Jhamat must find an extra £550 per month. They were able to purchase "a house we wouldn't have been able to afford" because they bought their home during the stamp duty holiday. .

According to Mr. Jhamat, "We assumed interest rates would remain low; otherwise, we would have taken out a five-year fix.". "It's wonderful to have hindsight. ".

The pharmacist's wife, a digital manager, and they must also come up with £1,000 each month for their one-year-old son's daycare costs. "Where we are now, we've wasted the savings we had on stamp duty.". We're essentially starting over," he said.

For many people, paying a mortgage is their largest monthly expense, so choosing the right product requires careful consideration and expert advice.

The issue is that lenders have recently started to abruptly discontinue their mortgage products. A frantic situation results from that.

Brokers were notified by HSBC on Thursday that it would cancel its deals four hours later. It quickly withdrew applications after receiving a flood of them, only to temporarily reopen the application channel on Friday.

Big lenders only want as many applications as they can handle in these circumstances; they do not want their deals to be significantly less expensive than those of their competitors.

"These last-minute communications just add to the stress of the situation," said Justin Moy, founder of Chelmsford-based mortgage broker EHF Mortgages. Especially when the increases are significant and have a significant impact on a borrower, decisions about rate changes and repricing must give everyone the chance to react calmly. ".

Homeowners who decide the best course of action is to do nothing and wait for things to calm down risk receiving a nasty shock.

A borrower automatically switches to their lender's standard variable rate (SVR) when a fixed term expires, which typically happens after two or five years. The majority of people instead move on to another fixed deal because the rate is higher; however, not everyone has that option because, for instance, they might have previously missed payments.

Brokers claim that because these SVRs have increased, anyone who chooses to wait and see will experience a significant increase in their rate, which will result in a significantly higher monthly mortgage payment.

Compared to other lenders, some have much higher SVRs. When their rates expire, we advise our clients to choose a lender that treats its clients fairly, according to broker Trinity Financial's Aaron Strutt.

Because they had become so accustomed to extremely low interest rates for the previous decade or more, many people were taken aback by the increase in mortgage rates that began in December 2021.

Interest rates were kept low, sometimes at historic lows, for a variety of economic and pandemic reasons.

Anyone who purchased their first home during that period would not have encountered this situation. Rates have been much higher in previous decades, but as house prices have risen, people are now borrowing more.

Lenders examined applicants' finances to determine whether they could handle higher interest rates. That is now more reality than theory, which may make some people wonder if they overextended themselves. Many people have avoided having to sell their homes, according to analysts, because of the availability of jobs and the low unemployment rate.

Tenants are also affected by it. Higher expenses for landlords will cause rental rates to rise, and if they decide to leave the industry, it will result in fewer homes being available for rent.

- You are formally in arrears if there is a shortfall that is equal to two or more months' worth of payments.

- Then, in order to treat you fairly, your lender must take into account any requests you make to modify your payment schedule, possibly with temporarily lower payments.

- Your ability to borrow money in the future will be impacted by any agreement you reach because it will appear on your credit report.

Visit this page for more information.

Jemma Dempsey contributed more reporting.